Seraphim Space Predictions 2024

1.Escalating geopolitical landscape intensifies global governments’ to bolster their independent space capabilities:

The worsening geopolitical environment has turbo-charged the desire of governments around the world to develop their own space capabilities. We predict that this push for ever greater space sovereignty – be it in sending astronauts into Space, procuring dedicated satellite constellations, or fostering domestic launch capabilities – will be one of the defining trends of 2024. The efforts of rival nations to establish a position of dominance in Space will also see geopolitical tensions extending into orbit, creating a new domain of ‘astro politics’ that will likely be played out on the front pages of newspapers throughout the year.

2.Department of Defence sourcing from the private sector propel ‘NewSpace’ market to unprecedented heights:

The steadfast commitment of the Department of Defence (DoD) to “buy what we can and build what we must” we expect to exert a profound influence in 2024. We anticipate a surge in contract awards reflecting the strategic imperative to harness cutting-edge technologies and innovations from agile and pioneering NewSpace companies with the DoD playing a pivotal. These DoD contracts will stimulate a cascading effect throughout the broader SpaceTech market. The increased investment and recognition from a key governmental player will likely attract additional private and institutional investors, fostering an environment conducive to sustained growth and innovation within the sector.

3.Further M&A consolidation, public markets to remain muted:

Anticipating robust activity in mergers and acquisitions (M&A) throughout 2024, we foresee a continuation of strategic moves from incumbents, ‘New Space’ leaders, and private equity players. The satcoms sector is poised for further consolidation as operators proactively fortify their defences against the looming threats posed by the ‘megaconstellations’ of Starlink, OneWeb, and Amazon Kuiper. Expectations of consolidation extend into the earth observation sector, driven by dual forces – a growing desire among government customers for multi-modal imaging/data fusion and the imperative for operators that went public through ill-fated SPAC-mergers to sustain and amplify revenue growth. The persistent price dislocation of publicly traded space stocks is likely to attract private equity buyers seeking potential price arbitrage opportunities, with an eye on privatizing some of these companies. While a certain degree of positive sentiment is anticipated to return to public markets, we do not envisage favourable conditions for space companies seeking to go public, barring the potential IPO of Starlink.

4.Sentiment in the space sector tied milestones achieved by SpaceX:

2024 is poised to be a pivotal year where SpaceX’s performance will act as the barometer for the entire space investment landscape. The spotlight will shine particularly bright on the much-anticipated Starship launch, with its success acting as a potential catalyst to galvanize and elevate investor optimism to new heights. Adding another layer of intrigue to the financial landscape is the prospect of Starlink, SpaceX’s satellite internet venture, going public. The mere contemplation of an initial public offering for Starlink has the potential to be nothing short of transformational for the space sector. Should this come to fruition, it could reshape the investment landscape, creating new opportunities and avenues for both institutional and retail investors. As such SpaceX will play a major role in shaping the trajectory of investor enthusiasm or caution in the ever-evolving space industry.

5.The Moon continues to be an important stepping stone to gain insights and access to our solar system. 2024 will see the next giant leap into a commercial lunar market:

We have witnessed four countries successfully achieving a moon landing to date, the United States, Russia, China and now India in 2023. It seems Japan will be hot on the heels in 2024. We predict a successful mission for Artemis II in the latter part of 2024 with NASA astronauts successfully circling the moon but not landing on the lunar South pole until 2025. Crucially, the Artemis programme is a government funded, commercially driven mission with NASA awarding contracts to established industry players like Lockheed Martin, and New Space giants like SpaceX, Blue Origin, and Firefly. They are also fostering the market much newer startups like Astrobotics, Intuitive Machines, and Zeno Power. We predict these companies will use the initial government support to launch commercially driven missions, opening up the moon for commercial activity.

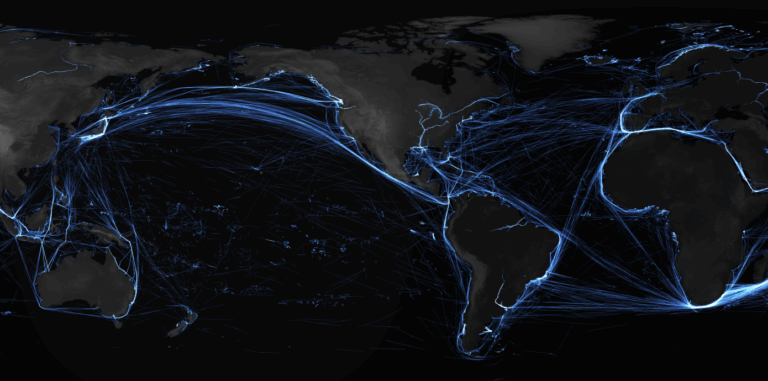

6 Regulatory Momentum to propel disclosure using Earth Observation data

The surge in regulatory measures aimed at enhancing climate disclosure is poised to act as a catalyst, propelling forward the Earth observation market. In 2023 California become the first U.S. state to enact mandatory climate emissions disclosure rules. As governments and regulatory bodies intensify their focus on environmental transparency and sustainability reporting, businesses and organisations are compelled to adopt data from advanced Earth observation satellites. Consequently, this regulatory momentum is expected to ignite unprecedented growth in the market, fostering the development and deployment of cutting-edge technologies that facilitate more accurate, independent, globally comparable metrics for monitoring of our planet’s vital signs. As the regulatory landscape evolves, so too will the Earth observation market, playing an important role in advancing our collective efforts towards a more sustainable and environmentally conscious future.

7.Return to Earth capabilities will start to unlock next phase of Space sector’s growth:

Just as low cost launch has reshaped the Space sector over the last decade, we anticipate that the advent of low cost, frequent return to Earth capabilities will have a similar impact over the next decade. We predict that 2024 will see the successful maiden missions for a number of pioneering companies that are developing their own capabilities for returning material from Space. This in turn will start to unlock the colossal potential of point-to-point delivery and space-based manufacturing.

8.Microgravity goldrush for advancements in life sciences and material sciences:

The microgravity realm of space isn’t just a scientific curiosity—it’s a potential goldmine for groundbreaking advancements in life sciences and material sciences. New classes of drugs and novel materials developed in Space could have a transformational impact on in areas as diverse as pharmaceuticals, telecoms and microelectronics. We predict that 2024 will be the year we start to see microgravity R&D move out of the lab, and off the International Space Station. We anticipate that during the year we will witness several companies making progress towards small scale production of materials formulated in space, including on free-flying platforms designed for in-space R&D and manufacturing.

9.VC investment in SpaceTech will continue its rebound:

Anticipating a sustained trajectory of recovery in VC investment levels over the upcoming quarters, we foresee this positive trend extending throughout 2024, buoyed by an overall improvement in market conditions. We predict that 2024 will be another year of record numbers of SpaceTech companies being funded, with both early and growth stage investment activity increasing. While the United States is poised to maintain its dominance in terms of total investment dollars, we forecast a significant uptick in investment levels within the United Kingdom, Europe, and Japan. This surge is expected to be catalysed by strategic initiatives from respective governments, underscoring a global expansion and diversification of venture capital interest and commitment in the SpaceTech sector.