TL;DR / Executive Summary

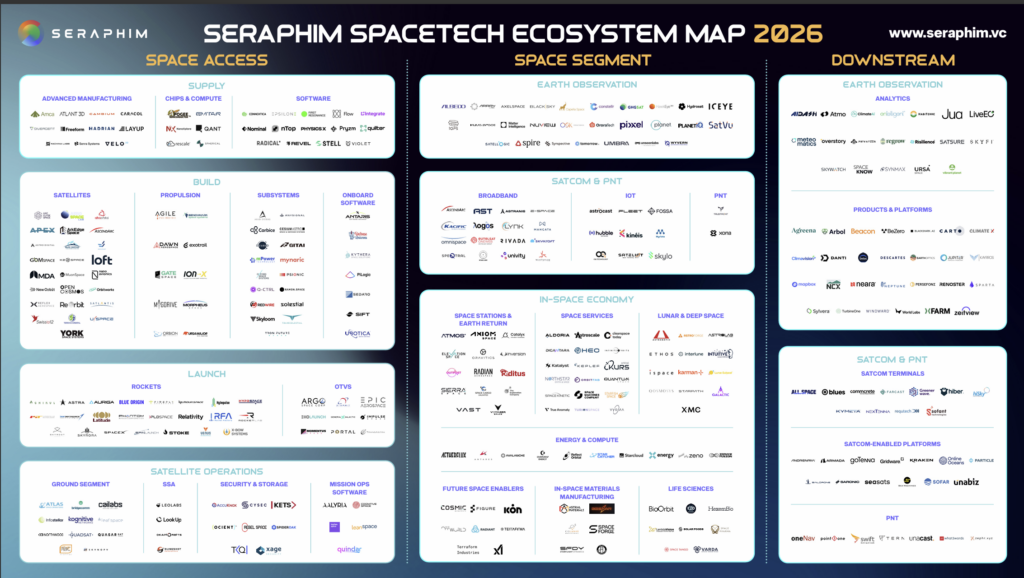

- Seraphim has released the SpaceTech Ecosystem Map 2026, covering 300+ companies and introducing a new three-layer framework.

- The model shifts from upstream versus downstream to Space Access, Space Segment, and Downstream, reflecting a more mature industry.

- New categories such as Supply, Satellite Operations, and the In-Space Economy highlight where innovation and investment are growing.

- The update clarifies how value is created, from infrastructure in orbit to products and services on Earth.

Since 2018, Seraphim has published its annual SpaceTech Ecosystem Map to bring structure and clarity to one of the fastest-evolving sectors in the global economy. Built on years of tracking thousands of companies and investment opportunities, the map highlights the most important, best-funded, and strategically significant players shaping the space economy.

Today, we are proud to release the Seraphim SpaceTech Ecosystem Map 2026, our most comprehensive and meaningful update to date.

Featuring over 300 companies across nine core categories, this year’s edition introduces a new three-layer framework and taxonomy, designed to better reflect how value is created across the modern space economy. This replaces the legacy “Upstream vs Downstream” model, which no longer fully captures the complexity or maturity of today’s market.

A New Three-Layer Framework

At the highest level, the ecosystem is now structured into three distinct layers:

1. Space Access

The foundational layer of the space economy. This includes everything required to get assets into orbit and keep them operational, from supply chains and manufacturing through to launch and satellite operations. It represents the industrial backbone enabling all space activity.

2. Space Segment

The in-orbit asset layer. This is where satellites and space-based infrastructure operate, generating data, delivering connectivity, and enabling entirely new economic activity. It is also the fastest-evolving part of the ecosystem, increasingly expanding beyond Earth orbit into cislunar and deep space.

3. Downstream

The monetisation layer. This is where space capabilities are translated into real-world products, services, and revenue on Earth. It represents the economic engine of the space sector, transforming data, connectivity, and positioning into tangible value across industries.

Why the Taxonomy Has Changed

The previous Upstream/Downstream framework served the industry well in its early stages. However, the space economy has now matured significantly:

- New infrastructure layers have emerged

- Value creation has shifted and diversified

- Entirely new categories of companies have scaled

The 2026 taxonomy reflects this evolution, providing a more accurate view of where innovation is happening and where value is being captured.

Key Taxonomy Updates

1. Supply: The Industrial Backbone Emerges

One of the most important additions is the creation of a dedicated Supply category within Space Access.

This segment captures companies providing critical components, advanced manufacturing, and software that enable space businesses, without building spacecraft themselves.

These businesses are increasingly vital as the industry shifts from innovation to scaled production. They also offer exposure to broader industrial tailwinds, including:

- Reindustrialisation and onshoring

- National security priorities

- AI-driven manufacturing transformation

Notably, many of these companies are founded by former SpaceX engineers, exporting world-class manufacturing and operational expertise into the wider industrial base.

2. Satellite Operations: A New Core Category

Previously fragmented across multiple areas, Satellite Operations is now recognised as a standalone vertical.

It includes all technologies required to manage and operate satellites in orbit, such as:

- Ground segment infrastructure

- Space situational awareness (SSA)

- Cybersecurity and secure communications

- Mission operations software

This reflects the growing importance of keeping space assets reliable, secure, and productive, without necessarily owning them.

3. In-Space Economy Comes of Age

What was once an emerging category has now become a core pillar of the ecosystem.

The In-Space Economy includes companies building and operating infrastructure beyond Earth, across areas such as:

- Space stations and in-orbit services

- Refuelling, repair, and debris removal

- Lunar and deep-space missions

- Space-based energy and compute

- In-space manufacturing and life sciences

This category has matured rapidly and now represents some of the most ambitious and well-funded opportunities in SpaceTech.

4. Introducing “Future Space Enablers”

Within the In-Space Economy, we introduce a new sub-category: Future Space Enablers.

These are companies that:

- Are not yet operating in space

- Are building commercially viable businesses on Earth today

- Have a clear roadmap toward enabling future space infrastructure

This includes technologies such as advanced robotics, energy systems, and resource processing, all essential for long-term, large-scale activity in space.

This category reflects a key belief: many of tomorrow’s space leaders are being built in terrestrial markets today.

5. A Reimagined Downstream Layer

The Downstream segment has been restructured to better reflect how value is now captured.

It is now divided into two core pillars:

Earth Observation – Products

Companies transforming satellite data into:

- Analytics and AI-driven insights

- Vertical SaaS platforms

- Decision-making tools across industries such as climate, agriculture, insurance, and logistics

Satcom & PNT – Products

A rapidly scaling ecosystem built on global connectivity and positioning, including:

- Terminals and hardware

- Connected platforms and edge devices

- Integrated applications and services

The expansion of low-cost satellite connectivity, particularly through LEO constellations, is unlocking entirely new markets, with sectors like maritime leading adoption.

A Clearer View of Value Creation

The updated framework provides a more intuitive way to understand the space economy:

- Space Access → enables access and operations

- Space Segment → owns and operates assets in orbit

- Downstream → captures economic value on Earth

This structure reflects the full lifecycle of value creation, from infrastructure to monetisation.

How to Use the Map

The Ecosystem Map is designed as a practical tool for the entire industry:

- Founders can identify adjacencies and whitespace opportunities

- Investors can track emerging themes and capital flows

- Corporates and governments can identify partners, suppliers, and acquisition targets

Conclusion

The space economy is entering a new phase, one defined not just by innovation, but by scale, infrastructure, and real economic output. The Seraphim SpaceTech Ecosystem Map 2026 reflects this transition. By introducing a more precise framework and taxonomy, we aim to provide a clearer lens on how the industry is evolving and where the most important opportunities lie.